Code

from sklearn.model_selection import train_test_split

train, test = train_test_split(ames, test_size = 0.25, random_state = 1234)This code deck assumes some basic knowledge of linear regression. Let’s review the basic concepts around linear regression:

Simple Linear Regression: one predictor variable for continuous target variable.

Multiple Linear Regression: two or more predictor variables (continuous or categorical) for continuous target variable.

Ordinary Least Squares: primary method of estimating linear regression where we find the regression line that minimizes the sum of the squares residuals (difference between prediction and truth).

For this analysis we are going to the popular Ames housing dataset. This dataset contains information on home values for a sample of nearly 1,500 houses in Ames, Iowa in the early 2000s. The data have already been reduced by removing variables using business logic, missingness, and low variability from the previous section.

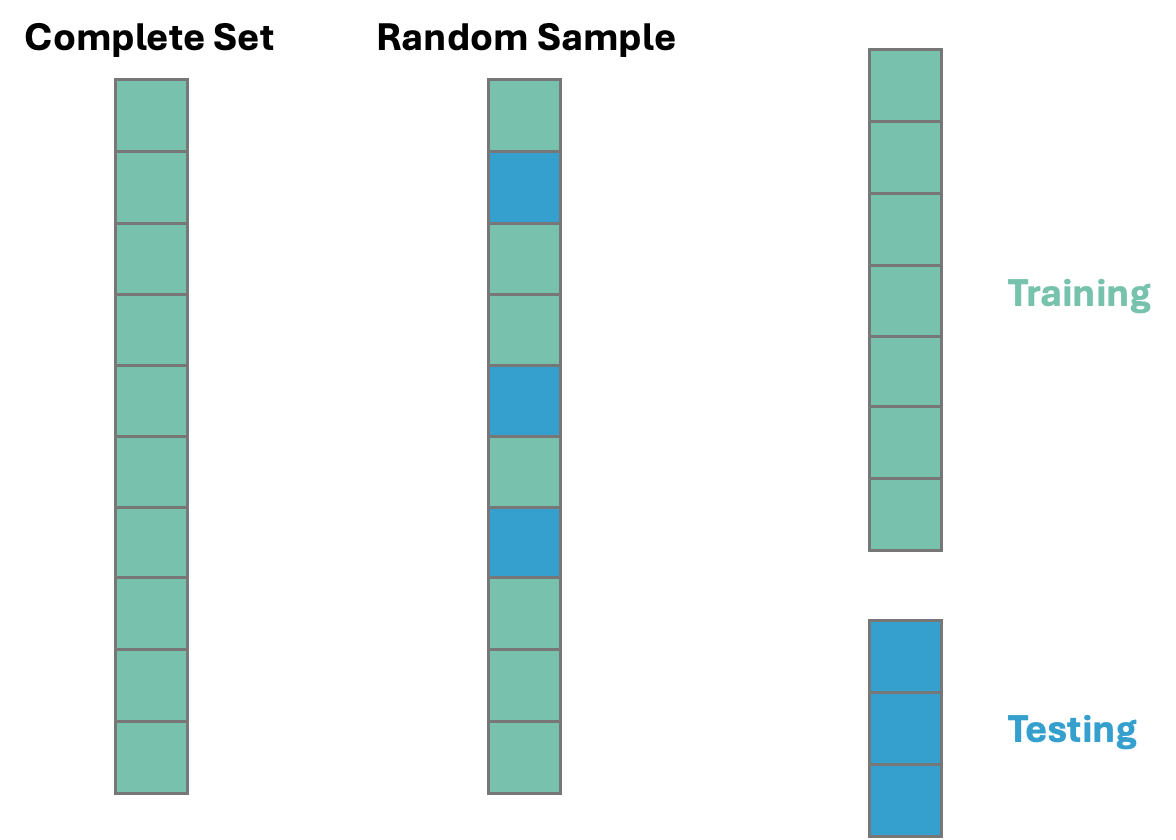

Before exploring any relationships between predictor variables and the target variable SalePrice, we need to split our data set into training and testing pieces. Because models are prone to discovering small, spurious patterns on the data that is used to create them (the training data), we set aside the testing data to get a clear view of how they might perform on new data that the models have never seen before.

from sklearn.model_selection import train_test_split

train, test = train_test_split(ames, test_size = 0.25, random_state = 1234)This split is done randomly. However, to make sure we can replicate this random split we use the random_state option. The data is split randomly so that the testing data set will approximate an honest assessment of how the model will perform in a real world setting. A visual representation of this is below:

Once we have our data split into training and testing datasets, we can now start to explore the relationships in the training data.

Before we start fully exploring our data we can now finish handling our missing values. We should not replace continuous predictor variable missing values on the whole dataset because that would impute the mean/median of the whole variable, not just the training data. We are not allowed to run any analysis on the whole dataset. This is especially the case if you wanted to impute missing values of a continuous variable using other variables in the dataset.

Let’s do this in each software!

The missing values from categorical predictor variables have already been imputed with a new category called Missing in the previous section. Therefore, we need to only look at the continuous variables for imputation at this stage. We isolate those variables using the select_dtypes function with the include = numeric option as well as the columns function.

num_cols = train.select_dtypes(include = 'number').columnsNow that we have a list of columns that are numerical in type we can loop through that list using a for loop. We identify any column that has missing values using the isnull and any functions after an if statement. Next, we create a missing value flag for that those columns in the loop based on the name of the variable using the isnull function. To convert these to the integer values of 0 and 1 we convert the type with the astype(int) function on that new variable. Lastly, we calculate the median of the variable of interest using the median function and then take that median calculation and put it in the fillna function to replace all the missing values in the variable. The loop continues this calculation for the rest of the variables.

for col in num_cols:

if train[col].isnull().any():

# Create missing flag column

train[f'{col}_was_missing'] = train[col].isnull().astype(int)

# Impute with median

median = train[col].median()

train[col] = train[col].fillna(median)Now our data is ready to explore!

To make sure we are getting the same data to analyze in R, we will import the Python train and test datasets. However, something similar can be done in R using the sample_frac function from the tidyverse package using the following code:

library(tidyverse)

ames <- ames %>% mutate(id = row_number())

set.seed(4321)

training <- ames %>% sample_frac(0.7)

testing <- anti_join(ames, training, by = 'id')Again, the above code was not run. The train and test datasets from Python were imported to make the analysis comparable.

train <- py$train

test <- py$testThe missing values from categorical predictor variables have already been imputed with a new category called Missing in the previous section. Therefore, we need to only look at the continuous variables for imputation at this stage. We isolate those variables using the sapply function with the is,numeric function within it.

num_cols <- names(train)[sapply(train, is.numeric)]Now that we have a list of columns that are numerical in type we can loop through that list using a for loop. We identify any column that has missing values using the is.na and any functions after an if statement. Next, we create a missing value flag for that those columns in the loop based on the name of the variable using the paste0 function. To convert these to the integer values of 0 and 1 we convert the type with the as.integer function on the variables identified with the is.na function. Lastly, we calculate the median of the variable of interest using the median function and then take that median calculation and put it in the is.na function with specific double [[ and ]] to replace all the missing values in the variable. The loop continues this calculation for the rest of the variables.

for (col in num_cols) {

if (any(is.na(train[[col]]))) {

# Create a missing flag column

flag_col <- paste0(col, "_was_missing")

train[[flag_col]] <- as.integer(is.na(train[[col]]))

# Impute with median

median_value <- median(train[[col]], na.rm = TRUE)

train[[col]][is.na(train[[col]])] <- median_value

}

}Now our data is ready to explore!

Once we have data that is ready to explore relationships we can quickly explore some individual predictor variable relationships with our target variable. If we have a small list of variables, this can be done by looking over scatterplots between your continuous predictor variables and your continuous target and boxplots for categorical predictors variables with your continuous target. However, when the list of variables starts to get large this becomes a burden. In these scenarios we can use automated techniques to quickly evaluate basic relationships between our predictors and our target. A quick word of caution; any time you use automated techniques to quickly go through large lists of variables, there is a chance that a couple of variables with really complicated relationships might slip through these simple relationship screenings. We are hoping that the large number of variables will overcome this problem and we are left with a large number still to pick from. That is why with smaller numbers of variables, visual exploration is always preferred.

The approach we will take is to look at univariate statistical tests between one predictor variable at a time with our target variable. We will screen out variables with p-values that are too high. Initial p-value selection is a common approach to remove variables with very low linear predictive power with our continuous target variable. The cut-off for these p-values is a critical question. A lot of introductory statistical test use a cut-off of 0.05. Anything below that would be considered statistically significant and worth moving on to the next stage of model building. However, this is a common misconception. The original author of the p-value, hypothesis test approach used 0.05 for their sample sizes of 50. It has been shown since that larger sample sizes need far lower cut-offs (referred to as \(\alpha\)-levels) to be reasonable. These \(\alpha\)-levels correspond to the probability of making a Type I error - in our scenario, falsely thinking a variable is significant when it really is not.

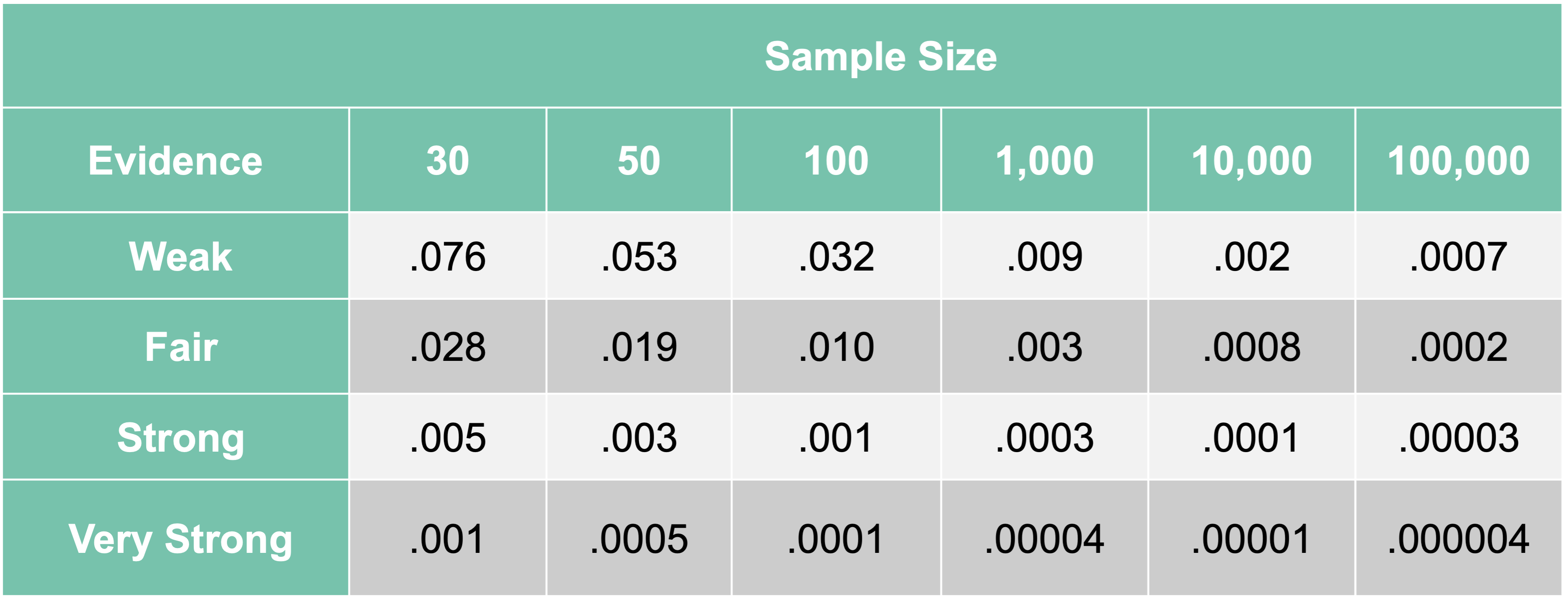

In a paper from 1994, Raftery provides more reasonable \(\alpha\)-levels based on sample size of the training dataset:

As we can see, an \(\alpha\)-level of 0.05 is good for sample sizes of about 50 for finding weak relationships. For the sample size of our data, a cut-off of about 0.009 is much more reasonable. We still want to find anything with at least a weak relationship with our target since we don’t want to be too restrictive this early on.

The p-value we use comes from the F-test from a simple linear regression. We will compare each individual variable in a simple linear regression with our target variable and record the F statistic p-value. The F-statistic is calculated as:

\[ F = \frac{MSR}{MSE} \]

where \(MSR\) refers to the mean square calculation from the regression model and \(MSE\) refers to the mean square calculation from the errors. More formally, \(MSR\) is the variance that is explained by the regression model. This is calculated by comparing the predictions from the regression model, \(\hat{y}_i\), to the overall average prediction, \(\bar{y}\):

\[ SSR = \sum_{i=1}^n (\hat{y}_i - \bar{y})^2 \]

This \(SSR\) is then divided by how many variables we have in the model, \(p\). In our scenario, \(p=1\). This can be thought of as the “average” of the variance explained per variable in the model.

This is then compared to the \(MSE\). The \(MSE\) is the variance that is unexplained from the model. This is calculated by comparing the true values of our target variable, \(y_i\), to our regression model’s predictions, \(\hat{y}_i\):

\[ SSE = \sum_{i=1}^n (y_i - \hat{y}_i)^2 \]

This \(SSE\) is then divided by the degrees of freedom in our error: \(n-p-1\). This can be thought of as the “average” amount of the remaining, unexplained variance per observation left over from our model.

Combining these together gives us our original F statistic:

\[ F = \frac{MSR}{MSE} = \frac{SSR/p}{SSE/(n-p-1)} \]

This ratio compares the amount of variation our model was able to explain (per variable) to how much variation is still left over (per observation). The more our model can explain, the larger this ratio becomes, which then makes our p-value smaller.

Let’s look at these automated approaches in each software!

Before we can put the predictor variables in our functions for automated screening we need to convert our categorical variables into dummy coded variables. Essentially, we need to one-hot encode our variables to make each category have a corresponding binary flag variable. Using the get_dummies function from Pandas we can do this easily. First, we must remove the target variable from our training data with the drop function. Just to make sure that all variables are of the same type, after converting the variables to binary flags we use the astype(float) function on all our predictor variables. Lastly, we call the predictor variables dataframe X and our target variable y.

import statsmodels.api as sm

# Dummy Code the Categorical Variables

predictors = train.drop(columns = ['SalePrice'])

predictors = pd.get_dummies(predictors, drop_first = True)

predictors = predictors.astype(float)

# Create Predictor and Target Objects

X = predictors

y = train['SalePrice']Once our data is in this format we can use the SelectKBest and f_regression functions from the popular sci-kit learn package, specifically sklearn.feature_selection. Inside SelectKBest we will use the f_regression function as our scoring function for each of the predictor variables. There are other options for a classification target if we had that instead. The k = 'all' option doesn’t eliminate any variables, but instead calculates the p-value for each variable. That way we can be the ones to decide which variables we want to keep. We then input our X and y objects into the fit function on the SelectKBest object. From there we just save the column names (columns), the test statistics (scores_), and p-values (pvalues_) into a single dataframe. We then use sort_values to sort in descending order by the F-statistic followed by printing them out to view.

from sklearn.feature_selection import SelectKBest, f_regression

# Fit SelectKBest but Show ALL Variables

selector = SelectKBest(score_func = f_regression, k = 'all')

selector.fit(X, y)SelectKBest(k='all', score_func=<function f_regression at 0x32ee92840>)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

| score_func | <function f_r...t 0x32ee92840> | |

| k | 'all' |

# Create a DataFrame with feature names, F-scores, and p-values

scores_df = pd.DataFrame({

'Feature': X.columns,

'F_score': selector.scores_,

'p_value': selector.pvalues_

})

# Sort by F-score descending

scores_df = scores_df.sort_values(by = 'F_score', ascending = False)

with pd.option_context('display.max_rows', None):

print(scores_df) Feature F_score p_value

2 OverallQual 1797.933303 4.305605e-233

8 GrLivArea 1083.918902 1.020195e-165

15 GarageCars 765.779731 3.526828e-128

16 GarageArea 679.101741 7.889357e-117

5 TotalBsmtSF 646.873094 1.818769e-112

6 1stFlrSF 640.245441 1.468943e-111

59 ExterQual_TA 555.825075 1.091141e-99

9 FullBath 477.720517 3.783999e-88

12 TotRmsAbvGrd 441.455145 1.361562e-82

76 KitchenQual_TA 402.015773 2.131390e-76

3 YearBuilt 386.023126 7.721397e-74

4 YearRemodAdd 381.849868 3.631354e-73

61 Foundation_PConc 375.129664 4.434457e-72

79 FireplaceQu_Missing 319.568158 6.755886e-63

13 Fireplaces 306.200382 1.240533e-60

14 GarageYrBlt 301.858406 6.818288e-60

68 BsmtQual_TA 275.524512 2.359938e-55

58 ExterQual_Gd 272.465749 8.051814e-55

86 GarageType_Detchd 168.736149 5.539706e-36

60 Foundation_CBlock 164.079394 4.229420e-35

82 GarageType_Attchd 151.637635 1.004137e-32

78 FireplaceQu_Gd 146.811156 8.512176e-32

0 LotFrontage 128.797978 2.682367e-28

18 OpenPorchSF 126.262795 8.419876e-28

7 2ndFlrSF 123.006569 3.672964e-27

72 HeatingQC_TA 119.599354 1.723333e-26

75 KitchenQual_Gd 114.516225 1.744797e-25

17 WoodDeckSF 111.941158 5.659995e-25

10 HalfBath 91.719347 6.435196e-21

30 LotShape_Reg 90.973468 9.112442e-21

1 LotArea 89.357988 1.937363e-20

97 GarageCond_TA 77.303445 5.596804e-18

54 HouseStyle_2Story 65.162272 1.806906e-15

73 CentralAir_Y 61.719648 9.424915e-15

84 GarageType_BuiltIn 57.950794 5.790911e-14

92 GarageQual_TA 57.457470 7.348571e-14

99 PavedDrive_Y 56.673698 1.073223e-13

87 GarageType_Missing 50.790290 1.863241e-12

95 GarageCond_Missing 50.790290 1.863241e-12

90 GarageQual_Missing 50.790290 1.863241e-12

27 GarageYrBlt_was_missing 50.790290 1.863241e-12

66 BsmtQual_Gd 49.776415 3.053328e-12

11 BedroomAbvGr 30.079500 5.149951e-08

74 KitchenQual_Fa 27.614571 1.779402e-07

67 BsmtQual_Missing 25.341035 5.614454e-07

34 LotConfig_CulDSac 25.236681 5.919311e-07

81 FireplaceQu_TA 24.333809 9.357904e-07

70 HeatingQC_Gd 23.388627 1.513049e-06

28 LotShape_IR2 21.719834 3.543780e-06

88 GarageQual_Fa 20.771390 5.757747e-06

93 GarageCond_Fa 18.677569 1.688980e-05

65 BsmtQual_Fa 18.280909 2.072552e-05

62 Foundation_Slab 17.987483 2.411733e-05

21 ScreenPorch 16.235861 5.979623e-05

19 EnclosedPorch 15.681304 7.981091e-05

47 BldgType_Duplex 15.621239 8.234931e-05

31 LandContour_HLS 15.582714 8.402011e-05

69 HeatingQC_Fa 15.385770 9.311052e-05

38 Condition1_Feedr 15.134336 1.061724e-04

57 ExterQual_Fa 14.806939 1.259915e-04

39 Condition1_Norm 13.551221 2.434765e-04

22 PoolArea 13.321565 2.747717e-04

48 BldgType_Twnhs 11.867634 5.928564e-04

50 HouseStyle_1.5Unf 11.011222 9.354708e-04

55 HouseStyle_SFoyer 10.087611 1.534472e-03

46 BldgType_2fmCon 9.241976 2.421586e-03

37 LotConfig_Inside 8.929279 2.869035e-03

98 PavedDrive_P 7.166567 7.538699e-03

85 GarageType_CarPort 7.156097 7.582535e-03

80 FireplaceQu_Po 5.439181 1.987078e-02

96 GarageCond_Po 4.885545 2.728904e-02

56 HouseStyle_SLvl 4.417574 3.579898e-02

42 Condition1_RRAe 3.376259 6.641335e-02

52 HouseStyle_2.5Fin 3.309407 6.915784e-02

91 GarageQual_Po 3.044455 8.129434e-02

89 GarageQual_Gd 2.364968 1.243759e-01

40 Condition1_PosA 2.253958 1.335620e-01

51 HouseStyle_1Story 2.245865 1.342607e-01

41 Condition1_PosN 1.984733 1.591771e-01

32 LandContour_Low 1.774032 1.831615e-01

83 GarageType_Basment 1.575615 2.096617e-01

20 3SsnPorch 1.496580 2.214620e-01

24 MoSold 1.415675 2.343749e-01

71 HeatingQC_Po 1.360606 2.436870e-01

25 YrSold 0.923403 3.367957e-01

53 HouseStyle_2.5Unf 0.900878 3.427561e-01

77 FireplaceQu_Fa 0.695147 4.046014e-01

45 Condition1_RRNn 0.666911 4.143088e-01

23 MiscVal 0.442107 5.062475e-01

36 LotConfig_FR3 0.402045 5.261676e-01

33 LandContour_Lvl 0.250091 6.171118e-01

63 Foundation_Stone 0.246604 6.195765e-01

26 LotFrontage_was_missing 0.222654 6.371196e-01

43 Condition1_RRAn 0.168449 6.815742e-01

29 LotShape_IR3 0.112438 7.374501e-01

94 GarageCond_Gd 0.091308 7.625783e-01

49 BldgType_TwnhsE 0.078756 7.790435e-01

35 LotConfig_FR2 0.005812 9.392463e-01

64 Foundation_Wood 0.004392 9.471704e-01

44 Condition1_RRNe 0.002970 9.565476e-01We now have a list of variables by their respective F-statistics and p-values. The OverallQual variable seems to be the most predictive.

From here we can remove the variables with a p-value above our 0.009 cut-off by isolating the specific variables that meet that requirement. We then select only those variables from our original X object to get our reduced variable list called X_reduced.

# Filter for features with p-value < 0.009

selected_features = scores_df[scores_df['p_value'] < 0.009]['Feature']

# Create a new DataFrame with only those selected columns

X_reduced = X[selected_features.tolist()]Before we can put the predictor variables in our functions for automated screening we need to convert our categorical variables into dummy coded variables. Essentially, we need to one-hot encode our variables to make each category have a corresponding binary flag variable. Using the model.matrix function we can do this easily. First, we must remove the target variable from our training data with the select function. Lastly, we call the predictor variables dataframe X and our target variable y.

library(broom)

library(dplyr)

# Create Predictor and Target Objects

y <- train$SalePrice

predictors <- train %>% select(-SalePrice)

# Dummy Code the Categorical Variables

X <- model.matrix(~ . - 1, data = predictors) %>% as.data.frame()

names(X)[names(X) == "`1stFlrSF`"] <- "FirstFlrSF"

names(X)[names(X) == "`2ndFlrSF`"] <- "SecondFlrSF"

names(X)[names(X) == "`3SsnPorch`"] <- "ThreeStoryPorch"Once our data is in this format we can use the lapply function and input our own function where we calculate the individual linear regressions. We will create our own function called feat where we calculate individual linear regressions with the lm function. From those individual regressions we use the summary function to extract the F-statistic information. From that information we can calculate the p-value using the pf function with the lower.tail = FALSE option. This approach doesn’t eliminate any variables, but instead calculates the p-value for each variable. That way we can be the ones to decide which variables we want to keep. We then use bind_rows to combine the information into a single data frame where we use desc to sort in descending order by the F-statistic followed by printing them out to view.

# Store feature names

features <- names(X)

# Loop through each feature, run univariate linear regression, and sort

scores_df <- lapply(features, function(feat) {

model <- lm(as.formula(paste("y ~", feat)), data = cbind(y = y, X))

f_val <- summary(model)$fstatistic

data.frame(

Feature = feat,

F_score = f_val[1],

p_value = pf(f_val[1], f_val[2], f_val[3], lower.tail = FALSE)

)

}) %>% bind_rows() %>%

arrange(desc(F_score))

# Print final result

print(scores_df) Feature F_score p_value

value...1 OverallQual 1.797933e+03 4.305605e-233

value...2 GrLivArea 1.083919e+03 1.020195e-165

value...3 GarageCars 7.657797e+02 3.526828e-128

value...4 GarageArea 6.791017e+02 7.889357e-117

value...5 TotalBsmtSF 6.468731e+02 1.818769e-112

value...6 FirstFlrSF 6.402454e+02 1.468943e-111

value...7 ExterQualTA 5.558251e+02 1.091141e-99

value...8 FullBath 4.777205e+02 3.783999e-88

value...9 TotRmsAbvGrd 4.414551e+02 1.361562e-82

value...10 KitchenQualTA 4.020158e+02 2.131390e-76

value...11 YearBuilt 3.860231e+02 7.721397e-74

value...12 YearRemodAdd 3.818499e+02 3.631354e-73

value...13 FoundationPConc 3.751297e+02 4.434457e-72

value...14 FireplaceQuMissing 3.195682e+02 6.755886e-63

value...15 Fireplaces 3.062004e+02 1.240533e-60

value...16 GarageYrBlt 3.018584e+02 6.818288e-60

value...17 BsmtQualTA 2.755245e+02 2.359938e-55

value...18 ExterQualGd 2.724657e+02 8.051814e-55

value...19 GarageTypeDetchd 1.687361e+02 5.539706e-36

value...20 FoundationCBlock 1.640794e+02 4.229420e-35

value...21 GarageTypeAttchd 1.516376e+02 1.004137e-32

value...22 FireplaceQuGd 1.468112e+02 8.512176e-32

value...23 LotFrontage 1.287980e+02 2.682367e-28

value...24 OpenPorchSF 1.262628e+02 8.419876e-28

value...25 SecondFlrSF 1.230066e+02 3.672964e-27

value...26 HeatingQCTA 1.195994e+02 1.723333e-26

value...27 KitchenQualGd 1.145162e+02 1.744797e-25

value...28 WoodDeckSF 1.119412e+02 5.659995e-25

value...29 HalfBath 9.171935e+01 6.435196e-21

value...30 LotShapeReg 9.097347e+01 9.112442e-21

value...31 LotArea 8.935799e+01 1.937363e-20

value...32 GarageCondTA 7.730344e+01 5.596804e-18

value...33 HouseStyle2Story 6.516227e+01 1.806906e-15

value...34 LotShapeIR1 6.189296e+01 8.671583e-15

value...35 CentralAirY 6.171965e+01 9.424915e-15

value...36 GarageTypeBuiltIn 5.795079e+01 5.790911e-14

value...37 GarageQualTA 5.745747e+01 7.348571e-14

value...38 PavedDriveY 5.667370e+01 1.073223e-13

value...39 GarageTypeMissing 5.079029e+01 1.863241e-12

value...40 GarageQualMissing 5.079029e+01 1.863241e-12

value...41 GarageCondMissing 5.079029e+01 1.863241e-12

value...42 GarageYrBlt_was_missing 5.079029e+01 1.863241e-12

value...43 BsmtQualGd 4.977642e+01 3.053328e-12

value...44 BedroomAbvGr 3.007950e+01 5.149951e-08

value...45 KitchenQualFa 2.761457e+01 1.779402e-07

value...46 BsmtQualMissing 2.534103e+01 5.614454e-07

value...47 LotConfigCulDSac 2.523668e+01 5.919311e-07

value...48 FireplaceQuTA 2.433381e+01 9.357904e-07

value...49 HeatingQCGd 2.338863e+01 1.513049e-06

value...50 LotShapeIR2 2.171983e+01 3.543780e-06

value...51 GarageQualFa 2.077139e+01 5.757747e-06

value...52 GarageCondFa 1.867757e+01 1.688980e-05

value...53 BsmtQualFa 1.828091e+01 2.072552e-05

value...54 FoundationSlab 1.798748e+01 2.411733e-05

value...55 ScreenPorch 1.623586e+01 5.979623e-05

value...56 EnclosedPorch 1.568130e+01 7.981091e-05

value...57 BldgTypeDuplex 1.562124e+01 8.234931e-05

value...58 LandContourHLS 1.558271e+01 8.402011e-05

value...59 HeatingQCFa 1.538577e+01 9.311052e-05

value...60 Condition1Feedr 1.513434e+01 1.061724e-04

value...61 ExterQualFa 1.480694e+01 1.259915e-04

value...62 Condition1Norm 1.355122e+01 2.434765e-04

value...63 PoolArea 1.332157e+01 2.747717e-04

value...64 BldgTypeTwnhs 1.186763e+01 5.928564e-04

value...65 HouseStyle1.5Unf 1.101122e+01 9.354708e-04

value...66 HouseStyleSFoyer 1.008761e+01 1.534472e-03

value...67 BldgType2fmCon 9.241976e+00 2.421586e-03

value...68 LotConfigInside 8.929279e+00 2.869035e-03

value...69 PavedDriveP 7.166567e+00 7.538699e-03

value...70 GarageTypeCarPort 7.156097e+00 7.582535e-03

value...71 FireplaceQuPo 5.439181e+00 1.987078e-02

value...72 GarageCondPo 4.885545e+00 2.728904e-02

value...73 HouseStyleSLvl 4.417574e+00 3.579898e-02

value...74 Condition1RRAe 3.376259e+00 6.641335e-02

value...75 HouseStyle2.5Fin 3.309407e+00 6.915784e-02

value...76 GarageQualPo 3.044455e+00 8.129434e-02

value...77 GarageQualGd 2.364968e+00 1.243759e-01

value...78 Condition1PosA 2.253958e+00 1.335620e-01

value...79 HouseStyle1Story 2.245865e+00 1.342607e-01

value...80 Condition1PosN 1.984733e+00 1.591771e-01

value...81 LandContourLow 1.774032e+00 1.831615e-01

value...82 GarageTypeBasment 1.575615e+00 2.096617e-01

value...83 ThreeStoryPorch 1.496580e+00 2.214620e-01

value...84 MoSold 1.415675e+00 2.343749e-01

value...85 HeatingQCPo 1.360606e+00 2.436870e-01

value...86 YrSold 9.234026e-01 3.367957e-01

value...87 HouseStyle2.5Unf 9.008783e-01 3.427561e-01

value...88 FireplaceQuFa 6.951470e-01 4.046014e-01

value...89 Condition1RRNn 6.669105e-01 4.143088e-01

value...90 MiscVal 4.421070e-01 5.062475e-01

value...91 LotConfigFR3 4.020451e-01 5.261676e-01

value...92 LandContourLvl 2.500908e-01 6.171118e-01

value...93 FoundationStone 2.466039e-01 6.195765e-01

value...94 LotFrontage_was_missing 2.226536e-01 6.371196e-01

value...95 Condition1RRAn 1.684491e-01 6.815742e-01

value...96 LotShapeIR3 1.124377e-01 7.374501e-01

value...97 GarageCondGd 9.130802e-02 7.625783e-01

value...98 BldgTypeTwnhsE 7.875602e-02 7.790435e-01

value...99 LotConfigFR2 5.811741e-03 9.392463e-01

value...100 FoundationWood 4.392474e-03 9.471704e-01

value...101 Condition1RRNe 2.970138e-03 9.565476e-01We now have a list of variables by their respective F-statistics and p-values. The OverallQual variable seems to be the most predictive.

From here we can remove the variables with a p-value above our 0.009 cut-off by isolating the specific variables that meet that requirement. We then select only those variables from our original X object to get our reduced variable list called X_reduced.

# Filter for features with p-value < 0.009

selected_features <- scores_df %>%

filter(p_value < 0.009) %>%

pull(Feature)

# Create a new data frame with only those selected columns

X_reduced <- X[, selected_features, drop = FALSE]Now we have a reduced list of variables from our data exploration. Before diving into model building concepts let’s build an initial model at our current state.

Now that we have a shorter variable list, let’s build an initial multiple linear regression model:

\[ \hat{y}_i = \hat{\beta}_0 + \hat{\beta}_1 x_{1,i} + \cdots + \hat{\beta}_p x_{p,i} \]

Once we take a look at this initial linear regression, then we will evaluate which variables we want to keep.

Let’s see how to do this in each of our software!

Before building a model in Python using the statsmodels.api package, we need to add a column of all 1’s. This column of all 1’s will create the intercept term, \(\beta_0\), in the linear regression. To do this we use the add_constant function on our reduced predictor variable dataframe. From there we just input the target variable and our predictor variables into the OLS function from statsmodels.api. The fit function will then fit our respective linear regression. Lastly, we use the summary function to view the output.

import statsmodels.api as sm

X_reduced = sm.add_constant(X_reduced)

model = sm.OLS(y, X_reduced)

result = model.fit()

print(result.summary()) OLS Regression Results

==============================================================================

Dep. Variable: SalePrice R-squared: 0.829

Model: OLS Adj. R-squared: 0.818

Method: Least Squares F-statistic: 75.26

Date: Sat, 15 Nov 2025 Prob (F-statistic): 0.00

Time: 10:50:47 Log-Likelihood: -12977.

No. Observations: 1095 AIC: 2.609e+04

Df Residuals: 1028 BIC: 2.642e+04

Df Model: 66

Covariance Type: nonrobust

===========================================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------------------

const -8.745e+04 2.54e+05 -0.344 0.731 -5.86e+05 4.11e+05

OverallQual 1.243e+04 1529.620 8.126 0.000 9427.513 1.54e+04

GrLivArea 1.0898 23.844 0.046 0.964 -45.699 47.879

GarageCars 1.339e+04 3624.893 3.694 0.000 6276.531 2.05e+04

GarageArea 25.8692 11.854 2.182 0.029 2.609 49.129

TotalBsmtSF 13.2116 6.415 2.059 0.040 0.623 25.800

1stFlrSF 37.1809 24.551 1.514 0.130 -10.994 85.356

ExterQual_TA -1.643e+04 8375.482 -1.961 0.050 -3.29e+04 9.692

FullBath 2177.6897 3377.463 0.645 0.519 -4449.820 8805.199

TotRmsAbvGrd 2150.1420 1458.739 1.474 0.141 -712.304 5012.588

KitchenQual_TA -3.76e+04 6384.526 -5.890 0.000 -5.01e+04 -2.51e+04

YearBuilt 183.5406 99.159 1.851 0.064 -11.036 378.117

YearRemodAdd 136.7789 83.252 1.643 0.101 -26.585 300.143

Foundation_PConc 1.391e+04 5578.347 2.494 0.013 2968.437 2.49e+04

FireplaceQu_Missing 2719.7438 7145.154 0.381 0.704 -1.13e+04 1.67e+04

Fireplaces 1.127e+04 4350.193 2.592 0.010 2738.713 1.98e+04

GarageYrBlt -261.6592 92.929 -2.816 0.005 -444.012 -79.306

BsmtQual_TA -3.679e+04 6601.991 -5.573 0.000 -4.97e+04 -2.38e+04

ExterQual_Gd -1.173e+04 7482.799 -1.568 0.117 -2.64e+04 2953.250

GarageType_Detchd 9558.9692 9097.893 1.051 0.294 -8293.592 2.74e+04

Foundation_CBlock 1.342e+04 4979.062 2.695 0.007 3648.407 2.32e+04

GarageType_Attchd 1.226e+04 8993.147 1.363 0.173 -5387.657 2.99e+04

FireplaceQu_Gd -7087.3241 5448.909 -1.301 0.194 -1.78e+04 3604.929

LotFrontage -35.6152 62.515 -0.570 0.569 -158.287 87.056

OpenPorchSF -17.6777 17.953 -0.985 0.325 -52.906 17.551

2ndFlrSF 53.1360 24.650 2.156 0.031 4.765 101.507

HeatingQC_TA -6243.5810 3274.991 -1.906 0.057 -1.27e+04 182.849

KitchenQual_Gd -3.022e+04 5638.921 -5.360 0.000 -4.13e+04 -1.92e+04

WoodDeckSF 33.4070 9.319 3.585 0.000 15.120 51.694

HalfBath 919.7145 3260.459 0.282 0.778 -5478.201 7317.630

LotShape_Reg -3858.9488 2546.583 -1.515 0.130 -8856.043 1138.145

LotArea 0.1977 0.142 1.395 0.163 -0.080 0.476

GarageCond_TA 1.133e+04 1.11e+04 1.021 0.307 -1.04e+04 3.31e+04

HouseStyle_2Story -1.476e+04 4711.293 -3.133 0.002 -2.4e+04 -5516.886

CentralAir_Y 2660.7298 5988.337 0.444 0.657 -9090.031 1.44e+04

GarageType_BuiltIn 1.077e+04 1.04e+04 1.033 0.302 -9691.479 3.12e+04

GarageQual_TA -1.946e+04 1.05e+04 -1.853 0.064 -4.01e+04 1151.166

PavedDrive_Y 3224.5206 5564.756 0.579 0.562 -7695.056 1.41e+04

GarageType_Missing 8484.6693 3962.121 2.141 0.032 709.900 1.63e+04

GarageCond_Missing 8484.6693 3962.121 2.141 0.032 709.900 1.63e+04

GarageQual_Missing 8484.6693 3962.121 2.141 0.032 709.900 1.63e+04

GarageYrBlt_was_missing 8484.6693 3962.121 2.141 0.032 709.900 1.63e+04

BsmtQual_Gd -3.593e+04 5316.082 -6.758 0.000 -4.64e+04 -2.55e+04

BedroomAbvGr -1692.3586 2087.286 -0.811 0.418 -5788.186 2403.468

KitchenQual_Fa -3.751e+04 9832.196 -3.815 0.000 -5.68e+04 -1.82e+04

BsmtQual_Missing -2.512e+04 1.66e+04 -1.513 0.131 -5.77e+04 7458.243

LotConfig_CulDSac 1.241e+04 5473.956 2.266 0.024 1664.626 2.31e+04

FireplaceQu_TA -5272.0765 5524.834 -0.954 0.340 -1.61e+04 5569.164

HeatingQC_Gd -4929.1065 3348.159 -1.472 0.141 -1.15e+04 1640.900

LotShape_IR2 1.384e+04 6924.985 1.998 0.046 249.567 2.74e+04

GarageQual_Fa -2.549e+04 1.2e+04 -2.123 0.034 -4.9e+04 -1933.388

GarageCond_Fa 1.142e+04 1.3e+04 0.875 0.382 -1.42e+04 3.7e+04

BsmtQual_Fa -4.171e+04 9989.190 -4.176 0.000 -6.13e+04 -2.21e+04

Foundation_Slab 2737.4065 1.71e+04 0.160 0.873 -3.07e+04 3.62e+04

ScreenPorch 56.4523 19.636 2.875 0.004 17.921 94.983

EnclosedPorch 4.4598 19.374 0.230 0.818 -33.557 42.476

BldgType_Duplex -2.193e+04 7500.892 -2.924 0.004 -3.66e+04 -7212.060

LandContour_HLS 6639.3386 6447.555 1.030 0.303 -6012.533 1.93e+04

HeatingQC_Fa -2907.5365 7307.787 -0.398 0.691 -1.72e+04 1.14e+04

Condition1_Feedr -987.5563 6084.564 -0.162 0.871 -1.29e+04 1.1e+04

ExterQual_Fa -2.059e+04 1.46e+04 -1.411 0.159 -4.92e+04 8049.064

Condition1_Norm 1.247e+04 4066.459 3.068 0.002 4495.034 2.05e+04

PoolArea -76.3474 32.180 -2.373 0.018 -139.493 -13.202

BldgType_Twnhs -1.906e+04 7258.792 -2.626 0.009 -3.33e+04 -4820.314

HouseStyle_1.5Unf 5347.2965 1.04e+04 0.513 0.608 -1.51e+04 2.58e+04

HouseStyle_SFoyer 3841.6662 8117.844 0.473 0.636 -1.21e+04 1.98e+04

BldgType_2fmCon -1.267e+04 8102.544 -1.564 0.118 -2.86e+04 3230.109

LotConfig_Inside -600.4065 2769.771 -0.217 0.828 -6035.456 4834.643

PavedDrive_P 1252.2416 9240.160 0.136 0.892 -1.69e+04 1.94e+04

GarageType_CarPort 5815.4725 1.54e+04 0.378 0.705 -2.43e+04 3.6e+04

==============================================================================

Omnibus: 431.767 Durbin-Watson: 2.057

Prob(Omnibus): 0.000 Jarque-Bera (JB): 50780.630

Skew: -0.779 Prob(JB): 0.00

Kurtosis: 36.325 Cond. No. 1.28e+16

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The smallest eigenvalue is 1.4e-21. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.We can see that we still have a lot of variables left in out regression model. Even though individually those predictor variables were all significant, together that is no longer the case. In the next section we will discuss strategies to help reduce the variable list even further.

In R we just input the target variable and our predictor variables into the lm function using the formula framework. Here, having the formula y ~ . uses our defined target variable object y we defined earlier and all of the variables in the X_reduced dataframe. Lastly, we use the summary function to view the output.

model <- lm(y ~ ., data = X_reduced)

summary(model)

Call:

lm(formula = y ~ ., data = X_reduced)

Residuals:

Min 1Q Median 3Q Max

-346458 -14779 399 13884 270746

Coefficients: (3 not defined because of singularities)

Estimate Std. Error t value Pr(>|t|)

(Intercept) -2.708e+05 2.527e+05 -1.071 0.284205

OverallQual 1.236e+04 1.509e+03 8.189 7.78e-16 ***

GrLivArea 1.218e+00 2.352e+01 0.052 0.958700

GarageCars 1.213e+04 3.583e+03 3.387 0.000735 ***

GarageArea 2.733e+01 1.170e+01 2.337 0.019623 *

TotalBsmtSF 1.694e+01 6.365e+00 2.661 0.007922 **

FirstFlrSF 3.743e+01 2.422e+01 1.546 0.122510

ExterQualTA -1.770e+04 8.265e+03 -2.142 0.032451 *

FullBath 1.347e+03 3.335e+03 0.404 0.686294

TotRmsAbvGrd 1.653e+03 1.442e+03 1.146 0.251871

KitchenQualTA -3.607e+04 6.304e+03 -5.721 1.39e-08 ***

YearBuilt 1.922e+02 9.783e+01 1.965 0.049660 *

YearRemodAdd 1.572e+02 8.221e+01 1.912 0.056188 .

FoundationPConc 1.274e+04 5.507e+03 2.313 0.020907 *

FireplaceQuMissing 1.992e+03 7.050e+03 0.283 0.777602

Fireplaces 1.162e+04 4.292e+03 2.708 0.006880 **

GarageYrBlt -2.428e+02 9.173e+01 -2.647 0.008257 **

BsmtQualTA -3.441e+04 6.527e+03 -5.272 1.65e-07 ***

ExterQualGd -1.296e+04 7.385e+03 -1.755 0.079565 .

GarageTypeDetchd 9.835e+03 8.975e+03 1.096 0.273375

FoundationCBlock 1.159e+04 4.923e+03 2.354 0.018783 *

GarageTypeAttchd 1.173e+04 8.872e+03 1.322 0.186359

FireplaceQuGd -7.917e+03 5.377e+03 -1.472 0.141237

LotFrontage 7.495e+00 6.218e+01 0.121 0.904081

OpenPorchSF -2.093e+01 1.772e+01 -1.181 0.237904

SecondFlrSF 5.415e+01 2.432e+01 2.227 0.026186 *

HeatingQCTA -6.312e+03 3.231e+03 -1.954 0.051011 .

KitchenQualGd -2.924e+04 5.565e+03 -5.255 1.80e-07 ***

WoodDeckSF 3.423e+01 9.194e+00 3.723 0.000207 ***

HalfBath 6.860e+02 3.217e+03 0.213 0.831153

LotShapeReg 8.535e+04 1.663e+04 5.134 3.40e-07 ***

LotArea 2.232e-01 1.400e-01 1.595 0.111092

GarageCondTA 1.211e+04 1.094e+04 1.107 0.268597

HouseStyle2Story -1.379e+04 4.651e+03 -2.964 0.003102 **

LotShapeIR1 9.014e+04 1.661e+04 5.428 7.11e-08 ***

CentralAirY 3.942e+02 5.922e+03 0.067 0.946937

GarageTypeBuiltIn 1.217e+04 1.029e+04 1.183 0.237129

GarageQualTA -1.884e+04 1.036e+04 -1.818 0.069354 .

PavedDriveY 1.764e+03 5.496e+03 0.321 0.748260

GarageTypeMissing 3.350e+04 1.563e+04 2.143 0.032349 *

GarageQualMissing NA NA NA NA

GarageCondMissing NA NA NA NA

GarageYrBlt_was_missing NA NA NA NA

BsmtQualGd -3.394e+04 5.257e+03 -6.456 1.66e-10 ***

BedroomAbvGr -1.598e+03 2.059e+03 -0.776 0.437822

KitchenQualFa -3.712e+04 9.699e+03 -3.827 0.000138 ***

BsmtQualMissing -2.031e+04 1.640e+04 -1.238 0.215872

LotConfigCulDSac 1.192e+04 5.400e+03 2.208 0.027461 *

FireplaceQuTA -6.296e+03 5.453e+03 -1.155 0.248530

HeatingQCGd -4.509e+03 3.304e+03 -1.365 0.172613

LotShapeIR2 1.022e+05 1.765e+04 5.789 9.39e-09 ***

GarageQualFa -2.503e+04 1.184e+04 -2.113 0.034800 *

GarageCondFa 1.125e+04 1.287e+04 0.874 0.382236

BsmtQualFa -3.538e+04 9.923e+03 -3.565 0.000380 ***

FoundationSlab 2.728e+03 1.683e+04 0.162 0.871257

ScreenPorch 5.447e+01 1.937e+01 2.812 0.005020 **

EnclosedPorch -2.149e+00 1.915e+01 -0.112 0.910686

BldgTypeDuplex -2.211e+04 7.399e+03 -2.989 0.002867 **

LandContourHLS 6.196e+03 6.361e+03 0.974 0.330231

HeatingQCFa -3.865e+03 7.211e+03 -0.536 0.592116

Condition1Feedr -9.217e+02 6.002e+03 -0.154 0.877988

ExterQualFa -2.252e+04 1.440e+04 -1.564 0.118136

Condition1Norm 1.175e+04 4.014e+03 2.928 0.003492 **

PoolArea -6.098e+01 3.187e+01 -1.913 0.055986 .

BldgTypeTwnhs -1.725e+04 7.168e+03 -2.407 0.016257 *

HouseStyle1.5Unf 5.480e+03 1.028e+04 0.533 0.594172

HouseStyleSFoyer 4.770e+03 8.010e+03 0.596 0.551631

BldgType2fmCon -1.369e+04 7.995e+03 -1.712 0.087230 .

LotConfigInside -3.196e+02 2.733e+03 -0.117 0.906929

PavedDriveP 9.922e+00 9.118e+03 0.001 0.999132

GarageTypeCarPort 5.518e+03 1.516e+04 0.364 0.715950

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 34530 on 1027 degrees of freedom

Multiple R-squared: 0.8333, Adjusted R-squared: 0.8224

F-statistic: 76.63 on 67 and 1027 DF, p-value: < 2.2e-16We can see that we still have a lot of variables left in out regression model. Even though individually those predictor variables were all significant, together that is no longer the case. In the next section we will discuss strategies to help reduce the variable list even further.

Just throwing all of our variables in a model, even if the list is reduced like we did above, is not the best strategy for model building. When it comes to model building there are a couple of things we need to consider - model metrics and selection algorithms.

Model metrics are evaluation calculations on models that we typically use to “select” variables for the model. Selection algorithms are automated techniques that quickly evaluate variables based on some selection criteria or model metric. There are two common types of algorithm groupings:

Stepwise Selection - step through decisions to build a model without evaluating every possible combination.

All-regression Selection - trying out all possible combinations of variables.

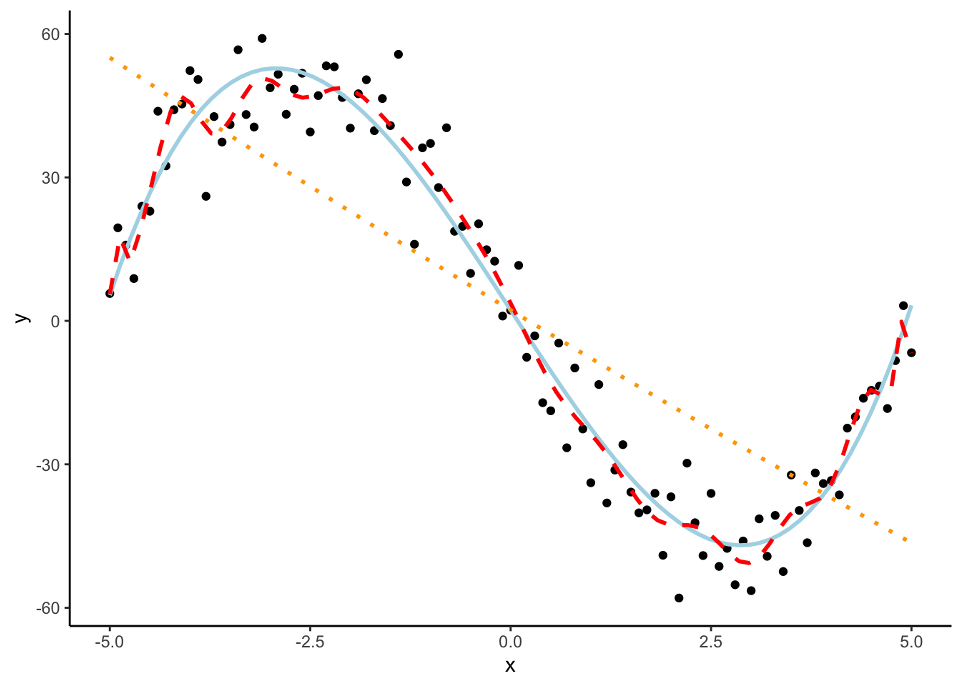

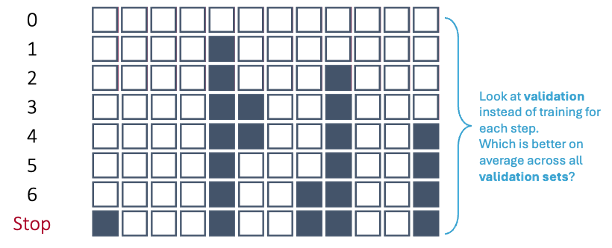

However, in the world of machine learning, we have a lot of aspects of a model that we need to “tune” or adjust to make our models more predictive. We can not perform this on the training data alone as it would lead to over-fitting (predicting too well) the training data and no longer be generalizable. Take the following plot:

The red line is overfitted to the dataset and picks up too much of the unimportant pattern. The orange dotted line is underfit as it does not pick up enough of the pattern. The light blue, solid line is fit well to the dataset as it picks up the general pattern while not overfitting to the dataset.

To help with over-fitting, we could split the training data set again into a training and validation data set where the validation data set is what we “tune” our models on. The downside of this approach is that we will tend to start over-fitting the validation data set.

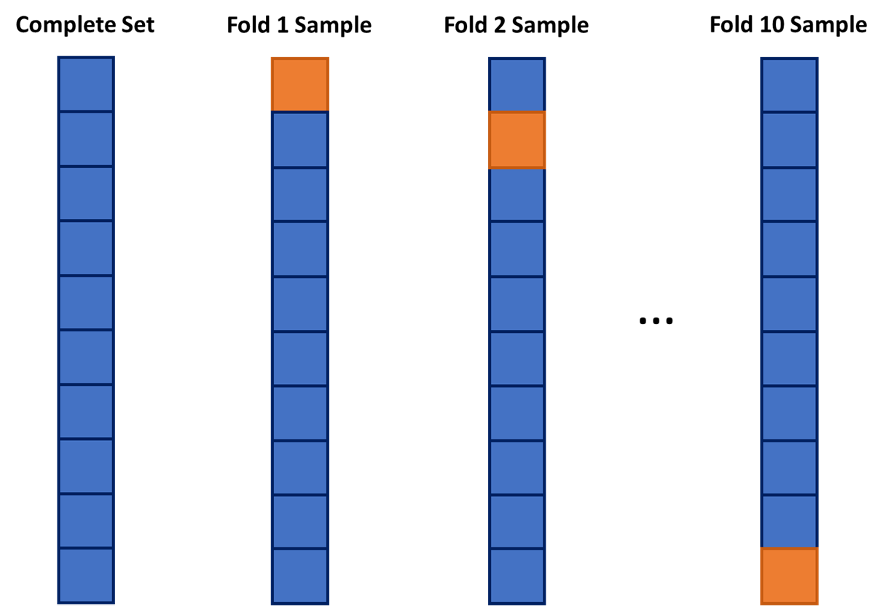

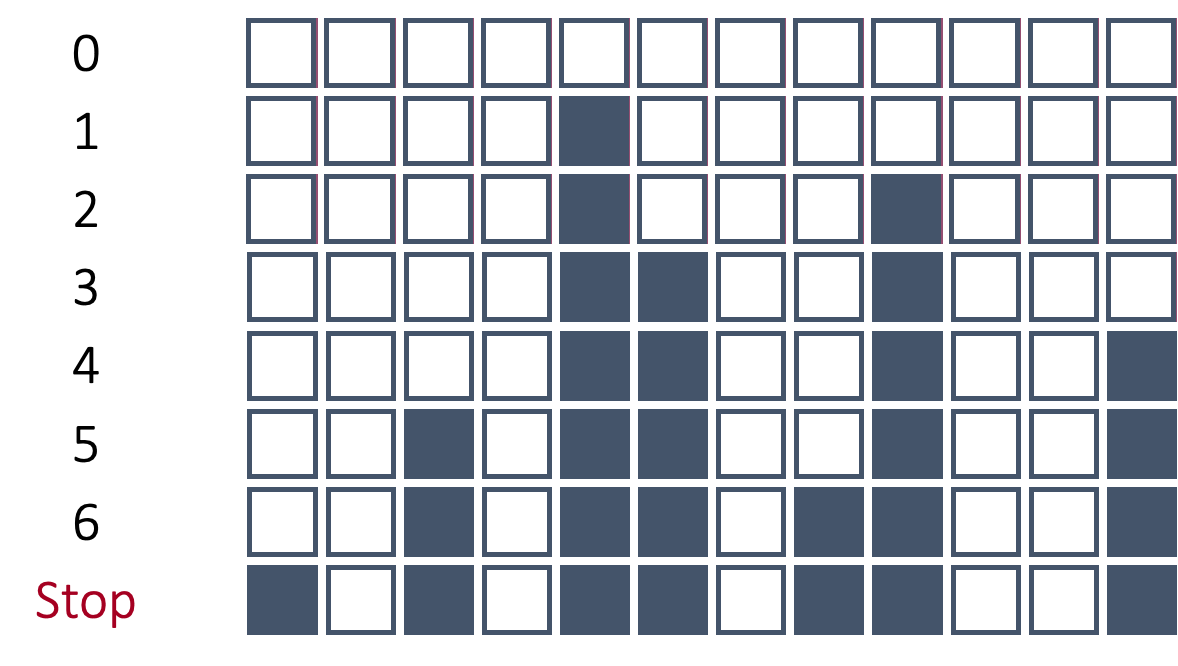

One approach to dealing with this is to use cross-validation. The idea of cross-validation is to divide your data set into k equally sized groups - called folds or samples. You leave one of the groups aside while building a model on the rest. You repeat this process of leaving one of the k folds out while building a model on the rest until each of the k folds has been left out once. We can evaluate a model by averaging the models’ effectiveness across all of the iterations. This process is highlighted below:

We will look at model building first without the use of cross-validation, but then with it.

Many different model metrics are used to help determine the validity of a model. Here of only SOME of the popular ones:

MAE (Mean Absolute Error) - the average of the absolute differences your predictions are from the truth.

MAPE (Mean Absolute Percentage Error) - the average of the absolute percentage differences your predictions are from the error.

MSE (Mean Squared Error) - the average of the squared differences your predictions are from the truth; also, the estimate of the variance of your errors from your model.

RMSE (Root Mean Squared Error) - the square root of the MSE; also, the standard deviation of your errors from your model.

In all of the above metrics, lower values represent a model that more highly predicts the target variable. However, these metrics might not always agree on which of the models is the best model.

Three of the above metrics are dependent on scale. Those metrics are the MAE, MSE, and RMSE:

Mean Absolute Error (MAE):

\[ MAE = \frac{1}{n} \sum_{i=1}^n |y_i - \hat{y}_i| \]

Mean Squared Error (MSE):

\[ MSE = \frac{1}{n} \sum_{i=1}^n (y_i - \hat{y}_i)^2 \]

Root Mean Squared Error (RMSE):

\[ RMSE = \sqrt(\frac{1}{n} \sum_{i=1}^n (y_i - \hat{y}_i)^2) \]

These metrics above are both scale dependent and symmetric. Scale dependent metrics are metrics that can only be compared to data with similar values for the data points. For example, we cannot compare a model trying to predict the price of a car with another model trying to predict the GDP of a country with MAE. An average error of $100,000 might be good for a model predicting GDP, but not as good for a model predicting price of a car. A symmetric metric is a metric that has the same meaning if the prediction is above the actual value as below the actual value. Again, for example, an error of $10,000 above a prediction is the same as an error $10,000 below a prediction.

The MAPE metric does not depend on scale, however, it is also not a symmetric metric.

Mean Absolute Percentage Error (MAPE):

\[ MAPE = \frac{1}{n} \sum_{i=1}^n |\frac{y_i - \hat{y}_i}{y_i}| \]

This final metric is both scale independent and asymmetric. Scale independent metrics are metrics that can be compared to data with any values for the data points. For example, we can compare a model trying to predict the price of a car with another model trying to predict the GDP of a country with MAPE. An average percentage error of 4% would be a worse model in context compared to a model with an average percentage error of 2.5%. An asymmetric metric is a metric that has a different meaning if the prediction is above the actual value as below the actual value. For example, a 5% error above is not the same as a 5% error below.

Which variables should you drop from your model? This is a common question for all modeling, but especially linear regression. In this section we will cover a popular variable selection technique - stepwise regression. This isn’t the only possible technique, but will be the primary focus here.

Stepwise regression techniques involve the three common methods:

Forward Selection

Backward Selection

Stepwise Selection

These techniques add or remove (depending on the technique) one variable at a time from your regression model to try and “improve” the model. There are a variety of different selection criteria to use to add or remove variables from a linear regression.

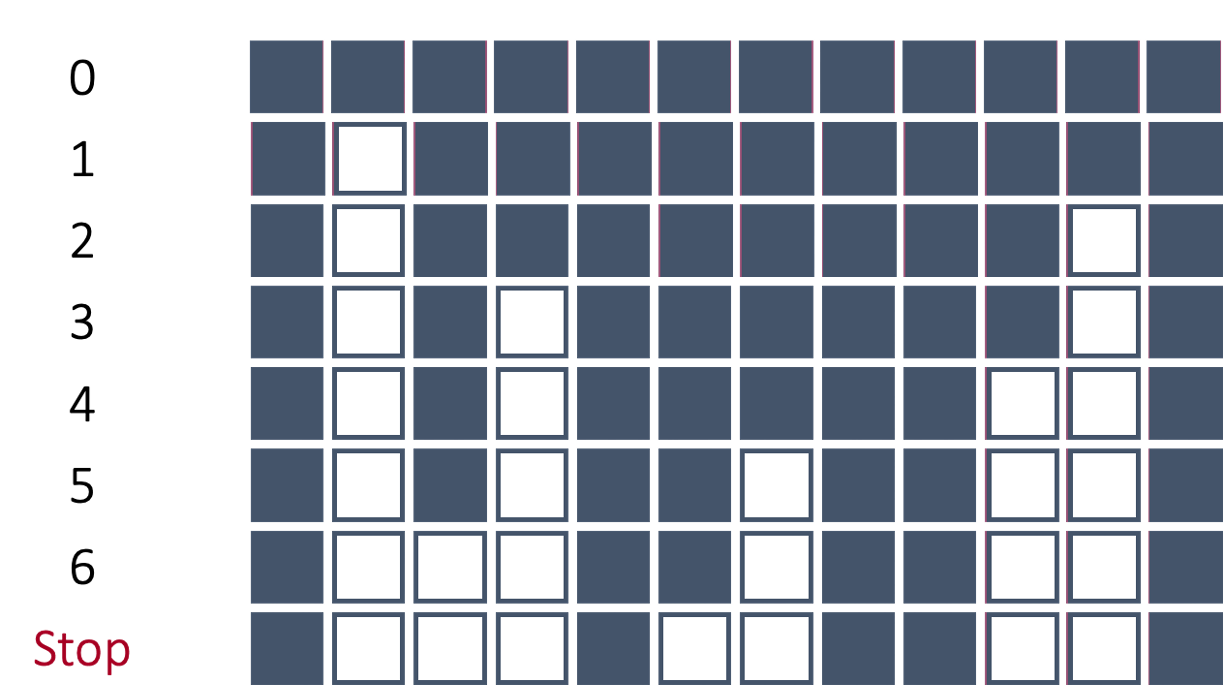

Let’s work through the process of forward selection. In forward selection, the initial model is empty (contains no variables, only the intercept). Each variable is then tried to see if it adds value based on a model metric. The variable that adds the most value is then added to the model. Then the remaining variables are again tested and the next most impactful variable is added to the model. This process repeats until either no more variables are available or no other variables improve the model metric.

Take a look at the picture below:

In the above example, after all of the variables were tested in models by themselves with the target, the 5th variable was deemed the best by the model metric. That variable is now in the model from this point forward. Next, all two variable models were built with every other variable added one at a time with the fifth variable. The combination of the 5th and 9th variables was deemed as the best combination from these options. Those two variables are now in the model going forward. This process stopped when no more variables improved the model metric on the overall model.

Forward selection is the least used technique because stepwise selection does the same as forward selection with an added benefit as discussed below.

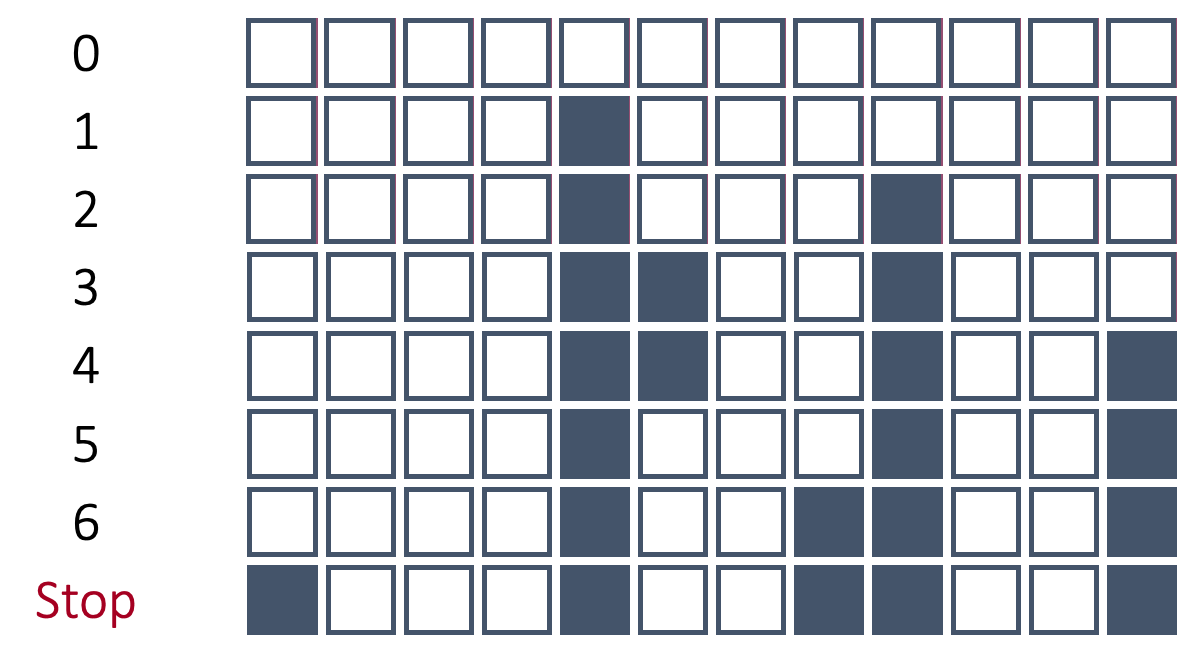

In backward selection, the initial model is full (contains all variables, including the intercept). Each variable is then tried to see if it is worth keeping based on a specific model metric. The least worthy variable (or the one that hinders the model the most) is then dropped from the model. Then the remaining variables are again tested and the next least important variable is dropped from the model.

Take a look at the picture below:

In the above example, the 2nd variable was deemed as the worst variable because the model improved the most (based on a model metric) with its deletion. Therefore, the 2nd variable is dropped from the model and cannot come back into the model. Next, each variable is again evaluated to see how the model improves with that variable’s deletion. The 11th variable is now deemed the worst and dropped. This process repeats until the model no longer improves with the deletion of another variable.

Backward selection is one of the most popular approaches to automatic model selection.

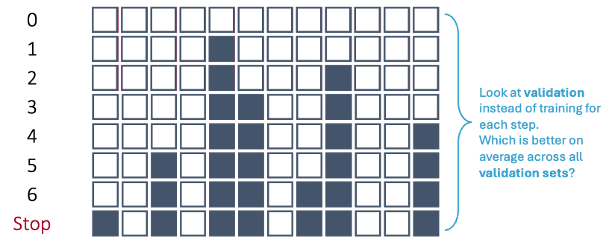

In stepwise selection, the initial model is empty (contains no variables, only the intercept) similar to forward selection. Each variable is then added one at a time to evaluate all single variable models to see which variable improves the model the most. The most important variable based on our model metric is then added to the model. Up until this point, it has been the same as forward selection. Next, all variables in the model (here only one) are tested to see if they are still helpful to the model by dropping all of them one at a time. This is similar to a backward selection at only this step. If they are hindering the model, they are dropped. Then the remaining variables are again tested and the next most impactful variable is added to the model. This process repeats until either no more variables are improving the model metric by adding or deleting variables.

Take a look at the picture below:

In the above picture the process starts off very similar to forward selection until we get to step 5. In step 5, the 6th variable is dropped from the model. In forward selection, if the 6th variable was added it could not be dropped. However, here that variable was evaluated to see if it still helped the model metric by being in the model. Since the model metric improved with the deletion of that variable, the variable was dropped.

All of the above techniques can be built with and without cross-validation. Both approaches are discussed in the following sections.

We will start without the use of cross-validation and only focusing on backward selection.

Let’s see how this works in each software!

Python has a built in recursive feature elimination (RFE) function inside of sklearn.feature_selection. However, there are some concerns with using that function. The biggest concern is the RFE function chooses variables in a linear regression based on the magnitude of the coefficients. This poses big problems in a linear regression model as we will see below.

First, let’s build a linear regression with the LinearRegression function from sklearn.linear_model and do backward selection with RFE. We put the LinearRegression object into the estimator option of the RFE function. Next, we need to figure out how many features we want to select. In the n_features_to_select option we can put any integer or the value of None. The None value will just select the “best” half of the variables from the model. From there we put our X_reduced and y objects in the fit function. Lastly, we get the variables from the RFE object with the support_ function and tie that to the respective variables using the columns function.

from sklearn.feature_selection import RFE

from sklearn.linear_model import LinearRegression

import pandas as pd

# Initialize model

model = LinearRegression()

# Set up Recursive Feature Elimination (RFE) to select top features

rfe = RFE(estimator = model, n_features_to_select = None)

rfe = rfe.fit(X_reduced, y)

# Get selected features

selected_features = X_reduced.columns[rfe.support_]

print("Selected features:", list(selected_features))Selected features: ['OverallQual', 'GarageCars', 'ExterQual_TA', 'FullBath', 'TotRmsAbvGrd', 'KitchenQual_TA', 'Foundation_PConc', 'FireplaceQu_Missing', 'Fireplaces', 'BsmtQual_TA', 'ExterQual_Gd', 'Foundation_CBlock', 'FireplaceQu_Gd', 'KitchenQual_Gd', 'HalfBath', 'GarageCond_TA', 'HouseStyle_2Story', 'GarageQual_TA', 'GarageType_Missing', 'GarageCond_Missing', 'GarageYrBlt_was_missing', 'BsmtQual_Gd', 'KitchenQual_Fa', 'BsmtQual_Missing', 'LotConfig_CulDSac', 'FireplaceQu_TA', 'LotShape_IR2', 'GarageQual_Fa', 'GarageCond_Fa', 'BsmtQual_Fa', 'BldgType_Duplex', 'ExterQual_Fa', 'Condition1_Norm', 'BldgType_Twnhs', 'BldgType_2fmCon']That is a long list of variables printed out above. Remember, this is only half of the variables because we specified the n_features_to_select = None option. Instead, let’s pick out the top 10 variables by changing that option.

# Initialize model

model = LinearRegression()

# Set up Recursive Feature Elimination (RFE) to select top features

rfe = RFE(estimator = model, n_features_to_select = 10)

rfe = rfe.fit(X_reduced, y)

# Get selected features

selected_features = X_reduced.columns[rfe.support_]

print("Selected features:", list(selected_features))Selected features: ['GarageCars', 'KitchenQual_TA', 'BsmtQual_TA', 'KitchenQual_Gd', 'BsmtQual_Gd', 'KitchenQual_Fa', 'BsmtQual_Missing', 'LotShape_IR2', 'BsmtQual_Fa', 'BldgType_Twnhs']Now that we a much more easily digestible list of the top 10 variables. One of the pitfalls of using the RFE function is that it doesn’t provide any notion of a cut-off based metric where all variables meeting a certain threshold are kept while others are eliminated. The choice of how many variables is completely up to the user.

Let’s examine what would happen if we change the scale of one of our variables. The OverallQual variable is on a scale of 1 to 10. Let’s change that scale to 0 to 1 by dividing that variable by 10. This doesn’t change any notion of the strength of the relationship between this variable at the target variable since we are just changing the scale. Let’s build a linear regression with this new dataset called X_new with our changed variable.

X_new = X_reduced.copy()

X_new['OverallQual'] = X_new['OverallQual']/10

model_new = sm.OLS(y, X_new).fit()

print(model_new.summary()) OLS Regression Results

==============================================================================

Dep. Variable: SalePrice R-squared: 0.829

Model: OLS Adj. R-squared: 0.818

Method: Least Squares F-statistic: 75.26

Date: Sat, 15 Nov 2025 Prob (F-statistic): 0.00

Time: 10:50:48 Log-Likelihood: -12977.

No. Observations: 1095 AIC: 2.609e+04

Df Residuals: 1028 BIC: 2.642e+04

Df Model: 66

Covariance Type: nonrobust

===========================================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------------------

const -8.745e+04 2.54e+05 -0.344 0.731 -5.86e+05 4.11e+05

OverallQual 1.243e+05 1.53e+04 8.126 0.000 9.43e+04 1.54e+05

GrLivArea 1.0898 23.844 0.046 0.964 -45.699 47.879

GarageCars 1.339e+04 3624.893 3.694 0.000 6276.531 2.05e+04

GarageArea 25.8692 11.854 2.182 0.029 2.609 49.129

TotalBsmtSF 13.2116 6.415 2.059 0.040 0.623 25.800

1stFlrSF 37.1809 24.551 1.514 0.130 -10.994 85.356

ExterQual_TA -1.643e+04 8375.482 -1.961 0.050 -3.29e+04 9.692

FullBath 2177.6897 3377.463 0.645 0.519 -4449.820 8805.199

TotRmsAbvGrd 2150.1420 1458.739 1.474 0.141 -712.304 5012.588

KitchenQual_TA -3.76e+04 6384.526 -5.890 0.000 -5.01e+04 -2.51e+04

YearBuilt 183.5406 99.159 1.851 0.064 -11.036 378.117

YearRemodAdd 136.7789 83.252 1.643 0.101 -26.585 300.143

Foundation_PConc 1.391e+04 5578.347 2.494 0.013 2968.437 2.49e+04

FireplaceQu_Missing 2719.7438 7145.154 0.381 0.704 -1.13e+04 1.67e+04

Fireplaces 1.127e+04 4350.193 2.592 0.010 2738.713 1.98e+04

GarageYrBlt -261.6592 92.929 -2.816 0.005 -444.012 -79.306

BsmtQual_TA -3.679e+04 6601.991 -5.573 0.000 -4.97e+04 -2.38e+04

ExterQual_Gd -1.173e+04 7482.799 -1.568 0.117 -2.64e+04 2953.250

GarageType_Detchd 9558.9692 9097.893 1.051 0.294 -8293.592 2.74e+04

Foundation_CBlock 1.342e+04 4979.062 2.695 0.007 3648.407 2.32e+04

GarageType_Attchd 1.226e+04 8993.147 1.363 0.173 -5387.657 2.99e+04

FireplaceQu_Gd -7087.3241 5448.909 -1.301 0.194 -1.78e+04 3604.929

LotFrontage -35.6152 62.515 -0.570 0.569 -158.287 87.056

OpenPorchSF -17.6777 17.953 -0.985 0.325 -52.906 17.551

2ndFlrSF 53.1360 24.650 2.156 0.031 4.765 101.507

HeatingQC_TA -6243.5810 3274.991 -1.906 0.057 -1.27e+04 182.849

KitchenQual_Gd -3.022e+04 5638.921 -5.360 0.000 -4.13e+04 -1.92e+04

WoodDeckSF 33.4070 9.319 3.585 0.000 15.120 51.694

HalfBath 919.7145 3260.459 0.282 0.778 -5478.201 7317.630

LotShape_Reg -3858.9488 2546.583 -1.515 0.130 -8856.043 1138.145

LotArea 0.1977 0.142 1.395 0.163 -0.080 0.476

GarageCond_TA 1.133e+04 1.11e+04 1.021 0.307 -1.04e+04 3.31e+04

HouseStyle_2Story -1.476e+04 4711.293 -3.133 0.002 -2.4e+04 -5516.886

CentralAir_Y 2660.7298 5988.337 0.444 0.657 -9090.031 1.44e+04

GarageType_BuiltIn 1.077e+04 1.04e+04 1.033 0.302 -9691.479 3.12e+04

GarageQual_TA -1.946e+04 1.05e+04 -1.853 0.064 -4.01e+04 1151.166

PavedDrive_Y 3224.5206 5564.756 0.579 0.562 -7695.056 1.41e+04

GarageType_Missing 8484.6693 3962.121 2.141 0.032 709.900 1.63e+04

GarageCond_Missing 8484.6693 3962.121 2.141 0.032 709.900 1.63e+04

GarageQual_Missing 8484.6693 3962.121 2.141 0.032 709.900 1.63e+04

GarageYrBlt_was_missing 8484.6693 3962.121 2.141 0.032 709.900 1.63e+04

BsmtQual_Gd -3.593e+04 5316.082 -6.758 0.000 -4.64e+04 -2.55e+04

BedroomAbvGr -1692.3586 2087.286 -0.811 0.418 -5788.186 2403.468

KitchenQual_Fa -3.751e+04 9832.196 -3.815 0.000 -5.68e+04 -1.82e+04

BsmtQual_Missing -2.512e+04 1.66e+04 -1.513 0.131 -5.77e+04 7458.243

LotConfig_CulDSac 1.241e+04 5473.956 2.266 0.024 1664.626 2.31e+04

FireplaceQu_TA -5272.0765 5524.834 -0.954 0.340 -1.61e+04 5569.164

HeatingQC_Gd -4929.1065 3348.159 -1.472 0.141 -1.15e+04 1640.900

LotShape_IR2 1.384e+04 6924.985 1.998 0.046 249.567 2.74e+04

GarageQual_Fa -2.549e+04 1.2e+04 -2.123 0.034 -4.9e+04 -1933.388

GarageCond_Fa 1.142e+04 1.3e+04 0.875 0.382 -1.42e+04 3.7e+04

BsmtQual_Fa -4.171e+04 9989.190 -4.176 0.000 -6.13e+04 -2.21e+04

Foundation_Slab 2737.4065 1.71e+04 0.160 0.873 -3.07e+04 3.62e+04

ScreenPorch 56.4523 19.636 2.875 0.004 17.921 94.983

EnclosedPorch 4.4598 19.374 0.230 0.818 -33.557 42.476

BldgType_Duplex -2.193e+04 7500.892 -2.924 0.004 -3.66e+04 -7212.060

LandContour_HLS 6639.3386 6447.555 1.030 0.303 -6012.533 1.93e+04

HeatingQC_Fa -2907.5365 7307.787 -0.398 0.691 -1.72e+04 1.14e+04

Condition1_Feedr -987.5563 6084.564 -0.162 0.871 -1.29e+04 1.1e+04

ExterQual_Fa -2.059e+04 1.46e+04 -1.411 0.159 -4.92e+04 8049.064

Condition1_Norm 1.247e+04 4066.459 3.068 0.002 4495.034 2.05e+04

PoolArea -76.3474 32.180 -2.373 0.018 -139.493 -13.202

BldgType_Twnhs -1.906e+04 7258.792 -2.626 0.009 -3.33e+04 -4820.314

HouseStyle_1.5Unf 5347.2965 1.04e+04 0.513 0.608 -1.51e+04 2.58e+04

HouseStyle_SFoyer 3841.6662 8117.844 0.473 0.636 -1.21e+04 1.98e+04

BldgType_2fmCon -1.267e+04 8102.544 -1.564 0.118 -2.86e+04 3230.109

LotConfig_Inside -600.4065 2769.771 -0.217 0.828 -6035.456 4834.643

PavedDrive_P 1252.2416 9240.160 0.136 0.892 -1.69e+04 1.94e+04

GarageType_CarPort 5815.4725 1.54e+04 0.378 0.705 -2.43e+04 3.6e+04

==============================================================================

Omnibus: 431.767 Durbin-Watson: 2.057

Prob(Omnibus): 0.000 Jarque-Bera (JB): 50780.630

Skew: -0.779 Prob(JB): 0.00

Kurtosis: 36.325 Cond. No. 1.28e+16

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The smallest eigenvalue is 1.4e-21. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.The model’s ability to predict the target variable has not changed at all. The \(R^2\) value, adjusted \(R^2\) value, Log-Likelihood value, and F-statistic are all the exact same. This should not be surprising as the variable really isn’t any different except for the scale change. However, let’s examine the coefficient on that OverallQual variable. Notice how that variable coefficient is now 10 times larger than it was in our original linear regression model from the previous section. The standard error is now 10 times bigger as well. However, since we divide those two to get the test statistic (t column), the test statistic is the exact same between this new regression and the original one. That means that the p-value on that variable between the two models is also the exact same.

So it appears that nothing has really changed! However, let’s run the RFE function again.

# Initialize model

model = LinearRegression()

# Set up Recursive Feature Elimination (RFE) to select top features

rfe = RFE(estimator = model, n_features_to_select = 10)

rfe = rfe.fit(X_new, y)

# Get selected features

selected_features = X_new.columns[rfe.support_]

print("Selected features:", list(selected_features))Selected features: ['OverallQual', 'KitchenQual_TA', 'BsmtQual_TA', 'KitchenQual_Gd', 'BsmtQual_Gd', 'KitchenQual_Fa', 'BsmtQual_Missing', 'LotShape_IR2', 'BsmtQual_Fa', 'BldgType_Twnhs']Notice how the OverallQual variable has now appeared in our top 10 list. But wait! I thought we just said that the model is no different and the variable has no different significance because the p-value did not change? Correct, but the coefficient did change because we changed the scale of the data. A variable’s coefficient in a linear regression is scale dependent because it is related to the interpretability of the variable. By changing the scale, we changed the interpretation, and unfortunately, the rankings of variables produced by the RFE function.

For this reason, I do not recommend using the RFE function for variable selection. One possible work around for this would be to scale the variables first. An example of that is shown below by building a pipeline (using the make_pipeline) function to standardize the variables first (StandardScaler) and then put them into the RFE function.

from sklearn.preprocessing import StandardScaler

from sklearn.feature_selection import RFE

from sklearn.linear_model import LinearRegression

from sklearn.pipeline import make_pipeline

# RFE with standardized features

model = LinearRegression()

pipeline = make_pipeline(StandardScaler(), RFE(model, n_features_to_select = 10))

pipeline.fit(X_reduced, y)Pipeline(steps=[('standardscaler', StandardScaler()),

('rfe',

RFE(estimator=LinearRegression(), n_features_to_select=10))])In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. | steps | [('standardscaler', ...), ('rfe', ...)] | |

| transform_input | None | |

| memory | None | |

| verbose | False |

| copy | True | |

| with_mean | True | |

| with_std | True |

| estimator | LinearRegression() | |

| n_features_to_select | 10 | |

| step | 1 | |

| verbose | 0 | |

| importance_getter | 'auto' |

LinearRegression()

| fit_intercept | True | |

| copy_X | True | |

| tol | 1e-06 | |

| n_jobs | None | |

| positive | False |

# Access selected features from the RFE step

rfe_step = pipeline.named_steps['rfe']

selected_features = X_reduced.columns[rfe_step.support_]

print("Selected features:", list(selected_features))Selected features: ['OverallQual', 'GarageCars', '1stFlrSF', 'KitchenQual_TA', 'Foundation_PConc', 'Foundation_CBlock', '2ndFlrSF', 'KitchenQual_Gd', 'BsmtQual_Gd', 'KitchenQual_Fa']Although better, this still doesn’t get around the problem of needing to select how many variables we want in the regression model. Also, since our variables are standardized, we have now lost some of the interpretability of the coefficients on the variables which is one of the biggest advantages to using linear regression. The coefficients are no longer telling what would happen with a single unit increase in a variable, but a single standard deviation increase in the variable. This makes interpretation for clients more challenging.

R has a built in step function that does recursive feature elimination such as backward selection. It uses likelihood based metrics to selection variables. We will use two of the most common ones: AIC and BIC (can also be referred to as SBC).

The AIC, or Akaike Information Criterion, was developed by statistician Hirotugu Akaike in the 1970’s and is defined by:

\[ AIC = n \log(\frac{SSE}{n}) + 2(p + 1) \]

In this case, the \(SSE\) is the sum of squared error from the model and \(2(p+1)\) is the “penalty”, where \(p\) is the number of variables in the model. A smaller AIC indicates a better model.

BIC, also known as the Bayesian Information Criterion (also called SBC or Schwarz Bayesian Information) was first developed by Gideon E. Schwarz, also back in the 1970’s and is defined by:

\[ BIC = n \log(\frac{SSE}{n}) + (p+1)\log (n) \]

In this case, “Likelihood” is the likelihood of the data and \((p+1)\log(n)\) is the “penalty”, where \(p\) is the number of variables in the model and \(n\) is the sample size. A smaller BIC indicates a better model.

To do backward elimination in R, you will use the step function. First, we need to define our full model (which is the model with all the predictor variables in it) similarly to how we did this above in our initial linear regression using the lm function. We must also define the lowest possible model (the intercept only model). To do this we can use the formula y ~ 1 to indicate that we want just the intercept term predicting the target variable. Inside of the step function we put our starting model, the full model, in first. For the scope of the model, you need to put the “smallest model” (using the lower option) to the “largest model” (using the upper option). The direction = "backward" option specifies that we want backward selection. The penalty (which indicates the criteria) can be controlled by defining the k option. A value of 2 will use the AIC criterion while a value of \(\log(n)\) will use the BIC criterion.

full_model <- lm(y ~ . , data = X_reduced)

empty_model <- lm(y ~ 1, data = X_reduced)

back_model <- step(full_model,

scope = list(lower = empty_model,

upper = full_model),

direction = "backward", k = 2, trace = FALSE)

summary(back_model)

Call:

lm(formula = y ~ OverallQual + GarageCars + GarageArea + TotalBsmtSF +

FirstFlrSF + ExterQualTA + KitchenQualTA + YearBuilt + YearRemodAdd +

FoundationPConc + Fireplaces + GarageYrBlt + BsmtQualTA +

ExterQualGd + FoundationCBlock + FireplaceQuGd + SecondFlrSF +

HeatingQCTA + KitchenQualGd + WoodDeckSF + LotShapeReg +

LotArea + HouseStyle2Story + LotShapeIR1 + GarageQualTA +

GarageTypeMissing + BsmtQualGd + KitchenQualFa + BsmtQualMissing +

LotConfigCulDSac + FireplaceQuTA + LotShapeIR2 + GarageQualFa +

BsmtQualFa + ScreenPorch + BldgTypeDuplex + ExterQualFa +

Condition1Norm + PoolArea + BldgTypeTwnhs + BldgType2fmCon,

data = X_reduced)

Residuals:

Min 1Q Median 3Q Max

-346812 -14460 103 13912 269635

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -3.904e+05 2.173e+05 -1.797 0.072661 .

OverallQual 1.253e+04 1.470e+03 8.525 < 2e-16 ***

GarageCars 1.298e+04 3.456e+03 3.755 0.000183 ***

GarageArea 2.263e+01 1.113e+01 2.034 0.042176 *

TotalBsmtSF 1.678e+01 6.078e+00 2.761 0.005866 **

FirstFlrSF 4.159e+01 6.579e+00 6.322 3.80e-10 ***

ExterQualTA -1.874e+04 8.106e+03 -2.312 0.020964 *

KitchenQualTA -3.708e+04 6.157e+03 -6.022 2.38e-09 ***

YearBuilt 2.276e+02 8.369e+01 2.720 0.006644 **

YearRemodAdd 1.725e+02 7.861e+01 2.195 0.028413 *

FoundationPConc 1.234e+04 5.141e+03 2.400 0.016586 *

Fireplaces 1.077e+04 3.118e+03 3.454 0.000575 ***

GarageYrBlt -2.211e+02 8.825e+01 -2.505 0.012393 *

BsmtQualTA -3.433e+04 6.234e+03 -5.507 4.58e-08 ***

ExterQualGd -1.387e+04 7.217e+03 -1.921 0.054942 .

FoundationCBlock 1.103e+04 4.461e+03 2.473 0.013554 *

FireplaceQuGd -7.672e+03 4.064e+03 -1.888 0.059335 .

SecondFlrSF 5.904e+01 4.680e+00 12.616 < 2e-16 ***

HeatingQCTA -4.091e+03 2.746e+03 -1.490 0.136549

KitchenQualGd -2.992e+04 5.391e+03 -5.549 3.63e-08 ***

WoodDeckSF 3.526e+01 8.817e+00 3.999 6.81e-05 ***

LotShapeReg 8.672e+04 1.614e+04 5.374 9.49e-08 ***

LotArea 2.264e-01 1.350e-01 1.677 0.093820 .

HouseStyle2Story -1.455e+04 4.337e+03 -3.356 0.000819 ***

LotShapeIR1 9.170e+04 1.614e+04 5.681 1.73e-08 ***

GarageQualTA -1.335e+04 8.800e+03 -1.518 0.129432

GarageTypeMissing 1.644e+04 1.098e+04 1.498 0.134550

BsmtQualGd -3.406e+04 5.108e+03 -6.668 4.19e-11 ***

KitchenQualFa -3.950e+04 9.302e+03 -4.246 2.36e-05 ***

BsmtQualMissing -1.910e+04 1.195e+04 -1.598 0.110277

LotConfigCulDSac 1.247e+04 4.777e+03 2.610 0.009182 **

FireplaceQuTA -6.522e+03 4.286e+03 -1.522 0.128414

LotShapeIR2 1.042e+05 1.722e+04 6.052 1.99e-09 ***

GarageQualFa -2.120e+04 1.047e+04 -2.025 0.043109 *

BsmtQualFa -3.518e+04 9.640e+03 -3.649 0.000276 ***

ScreenPorch 5.242e+01 1.875e+01 2.795 0.005279 **

BldgTypeDuplex -2.043e+04 6.659e+03 -3.067 0.002214 **

ExterQualFa -2.461e+04 1.379e+04 -1.785 0.074483 .

Condition1Norm 1.179e+04 3.156e+03 3.734 0.000198 ***

PoolArea -6.370e+01 3.036e+01 -2.098 0.036136 *

BldgTypeTwnhs -1.726e+04 6.617e+03 -2.609 0.009206 **

BldgType2fmCon -1.234e+04 7.683e+03 -1.607 0.108445

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 34280 on 1053 degrees of freedom

Multiple R-squared: 0.8316, Adjusted R-squared: 0.825

F-statistic: 126.8 on 41 and 1053 DF, p-value: < 2.2e-16From the list above we can see that the variables have been reduced down based on that AIC criterion. At each step the variable removed improved the model the most in that specific step by being the model that resulted in the lowest AIC value.

There are better options when it comes to doing forward, backward, and stepwise selection algorithms using cross-validation which is discussed in the next section.

Instead of looking at any of the stepwise regression techniques by using only the training data, from a machine learning standpoint, each step of the process is not evaluated on the training data, but on the cross-validation data sets. The model with the best average MSE (for example) in cross-validation is the one that moves on to the next step of the selection algorithm.

Let’s revisit the backward selection from above under this premise.

In first step of the backward selection process, we create models such that each model has exactly one predictor variable removed from it and calculate a model metric for each model. However, we do this across each cross-validation training set. For 10-fold cross-validation, that would be 10 separate first steps that create models removing only one variable. Next, we average the model metric across all training sets to see which is the worst variable. For example, the second variable is now the worst on average across all of the cross-validation datasets based on our model metric, not just the training set overall.

This same process is repeated across all of the steps until a final model is selected where removing any further variables does not improve the model based on the cross-validation model metrics.

Let’s see this in each software!

To gain the needed functionality for cross-validation recursive feature addition or subtraction, we need to use the mlxtend package on top of scikit-learn. Specifically, we will use the SequentialFeatureSelector function from mlxtend.feature_selection. Similar to before we will need to create our linear regression object with the LinearRegression function. This object will be an input to our SequentialFeatureSelector function called SFS from this point forward. In the k_features option we can put any integer value to set a certain number of features, the "best" option to pick the number of features that provides the best value of the model metric, or the "parsimonious" option to pick the number of features within one standard error of the true best model to try and make the model simpler. The forward = False option makes the function perform backward selection. The floating = False option means that once a variable is dropped it can no longer be added back to the model. The scoring option allows you to select your model metric. The options for a continuous target variable are the negative MSE, the negative RMSE, the negative MAE, and \(R^2\). The reason the first three are negative is that the function tries to maximize the optimization function. The cv option allows you to pick the number of cross-validation folds. Lastly, we just use the fit function with our predictor variables and target variable to fit the model. The variables are then printed below.

from mlxtend.feature_selection import SequentialFeatureSelector as SFS

from sklearn.linear_model import LinearRegression

lr = LinearRegression()

sfs = SFS(lr,

k_features = "best",

forward = False,

floating = False,

scoring = 'neg_mean_squared_error',

cv = 10)

sfs = sfs.fit(X_reduced, y)

selected_features = list(sfs.k_feature_names_)

print("Selected features:", selected_features)Selected features: ['const', 'OverallQual', 'GarageCars', '1stFlrSF', 'ExterQual_TA', 'KitchenQual_TA', 'YearBuilt', 'YearRemodAdd', 'Foundation_PConc', 'Fireplaces', 'GarageYrBlt', 'BsmtQual_TA', 'Foundation_CBlock', '2ndFlrSF', 'HeatingQC_TA', 'KitchenQual_Gd', 'WoodDeckSF', 'LotShape_Reg', 'HouseStyle_2Story', 'CentralAir_Y', 'GarageQual_TA', 'GarageType_Missing', 'GarageCond_Missing', 'GarageQual_Missing', 'GarageYrBlt_was_missing', 'BsmtQual_Gd', 'KitchenQual_Fa', 'BsmtQual_Missing', 'LotConfig_CulDSac', 'HeatingQC_Gd', 'LotShape_IR2', 'GarageQual_Fa', 'BsmtQual_Fa', 'ScreenPorch', 'BldgType_Duplex', 'ExterQual_Fa', 'Condition1_Norm', 'BldgType_Twnhs']Now we have variables determined by backward selection, but using cross-validation instead of just the whole training dataset.

To gain the needed functionality for cross-validation recursive feature addition or subtraction, we need to use the caret package. Specifically, we will use the train function from caret package along with the leaps package. The caret function can not handle our target variable and predictor variables being in separate objects. Therefore, we first use cbind to combine the target variable as a column to the predictor variables dataframe. Now we can use the new dataframe to put into caret with the typical formula structure we have used previously. The method = "leapBackward" option uses the leap package and its backward selection capabilities. You can think of caret as more of a wrapper function that puts a cross-validation spin on other functions. The tuneGrid option is where we specify what the model is tuning - here, the number of variables in the model. We are allowing that value to be anywhere from 1 variable all the way to 67 variables (the maximum amount we have). The metric option allows you to select your model metric. The options for a continuous target variable are the the RMSE, the MAE, and \(R^2\). The trControl = trainControl(method = 'cv', number = 10)) option allows you to pick the number of cross-validation folds. Lastly, we just look at the results element to view all of the possible model metrics across all tuning options and the bestTune element for it to tell us the optimal tuning value (optimal number of variables).

library(caret)

library(leaps)

set.seed(1234)

df <- cbind(y, X_reduced)

step_model <- caret::train(y ~ ., data = df,

method = "leapBackward",

tuneGrid = data.frame(nvmax = 1:67),

metric = "RMSE",

trControl = trainControl(method = 'cv',

number = 10))Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:Reordering variables and trying again:step_model$results nvmax RMSE Rsquared MAE RMSESD RsquaredSD MAESD

1 1 49977.95 0.6379845 34413.62 8212.437 0.04056464 3444.893

2 2 45459.07 0.7041046 30790.61 7926.356 0.06412756 2460.768

3 3 42465.75 0.7458165 27781.02 10450.149 0.08616763 3338.279

4 4 41511.86 0.7594901 27182.04 10922.164 0.08467277 3508.469

5 5 41232.78 0.7619850 27029.26 10724.738 0.08285458 3368.540

6 6 40515.83 0.7702644 26542.27 11085.117 0.08570367 3569.525

7 7 40557.45 0.7698225 26624.11 11118.410 0.08590971 3648.460

8 8 40973.91 0.7663612 26311.93 12328.873 0.09694029 3473.413

9 9 40920.45 0.7673650 26132.34 12368.379 0.09692516 3281.338

10 10 40891.75 0.7691093 26121.63 12982.862 0.10313762 3490.216

11 11 40407.44 0.7740602 25719.59 13149.909 0.10591740 3511.174

12 12 40086.49 0.7772255 25407.08 13189.867 0.10694073 3469.621

13 13 39920.99 0.7784748 25189.05 12924.188 0.10432318 3373.224

14 14 40055.09 0.7780948 25130.63 13664.794 0.11034048 3555.922

15 15 40027.19 0.7777532 25160.91 13713.477 0.10972704 3604.560

16 16 39952.86 0.7789035 25093.18 13907.709 0.11048947 3634.715

17 17 40130.90 0.7767144 25084.03 14285.208 0.11509638 3603.802

18 18 40144.12 0.7765038 25034.20 14387.396 0.11566260 3630.875

19 19 39945.66 0.7787613 24872.55 14549.435 0.11747833 3831.055

20 20 40063.67 0.7767741 24996.00 14397.179 0.11519606 3922.747

21 21 39969.37 0.7780789 24931.91 14486.828 0.11591690 3728.593

22 22 39953.99 0.7779197 24971.49 14551.285 0.11614572 3767.608

23 23 39785.69 0.7796607 24909.19 14533.895 0.11584043 3765.717

24 24 39916.94 0.7784775 24981.24 14426.799 0.11540880 3685.338

25 25 39699.18 0.7806454 24851.48 14528.324 0.11682734 3854.198

26 26 39704.56 0.7807152 24870.64 14608.020 0.11726875 3959.261

27 27 40416.33 0.7725864 24987.20 15544.998 0.12506026 4233.939

28 28 40383.56 0.7731801 24822.57 15512.248 0.12390513 4100.529

29 29 40305.45 0.7737329 24731.46 15470.632 0.12363976 4354.071

30 30 40056.99 0.7764172 24485.28 15399.939 0.12305452 4372.851

31 31 39986.16 0.7769655 24473.29 15501.730 0.12407998 4427.617

32 32 39982.40 0.7772986 24533.92 15370.374 0.12225357 4428.186

33 33 40078.20 0.7762794 24540.73 15471.316 0.12317933 4392.251

34 34 40072.85 0.7762712 24504.77 15519.193 0.12370677 4364.689

35 35 39994.33 0.7771654 24476.86 15587.080 0.12408588 4376.086

36 36 39875.70 0.7784654 24400.96 15459.717 0.12333587 4240.014

37 37 39826.02 0.7791110 24300.89 15446.524 0.12314726 4076.386

38 38 39782.30 0.7797330 24265.98 15455.216 0.12338025 4015.840

39 39 39650.56 0.7810700 24113.85 15499.395 0.12376346 4076.217

40 40 39632.19 0.7816386 24084.26 15486.285 0.12379773 4083.176

41 41 39598.18 0.7822372 24153.47 15466.681 0.12352486 4041.807

42 42 39622.24 0.7815976 24081.13 15540.767 0.12454139 4045.688